Pension Plan Reforms 2026: Proposed Changes for Future Retirees

Latest developments on Pension Plan Reforms 2026 are drawing national attention as the Canadian government advances proposals aimed at strengthening long-term retirement sustainability. Officials confirmed that ongoing enhancements to the Canada Pension Plan remain a central focus, with policymakers reviewing contribution structures, retirement income adequacy, and demographic pressures linked to an aging population.

In the field of retirement planning, analysts say the proposed reforms could significantly influence future retirees, particularly younger workers expected to contribute under updated CPP enhancement rules. Discussions continue around balancing higher contribution requirements with expanded long-term retirement benefits and financial stability for future generations.

What readers should monitor next includes federal and provincial negotiations, updated actuarial reports, and any announcements involving contribution rate adjustments or retirement age discussions. Experts also recommend closely following inflation trends and labour market conditions, as these factors are expected to shape the final direction of Canada’s pension reform strategy through 2026.

Understanding the Proposed Pension Plan Reforms 2026

The Canadian government’s proposed Pension Plan Reforms are a comprehensive package designed to address long-term financial projections for the national pension system. These reforms are not isolated changes but rather a strategic response to demographic shifts, including increased life expectancy and fluctuating economic growth rates across the country.

Officials assert that these adjustments are critical to maintaining the solvency and fairness of the pension system for generations to come. The proposals aim to ensure that the plan can continue to provide reliable income to retirees while adapting to new societal realities and economic pressures.

The specifics of the reforms touch upon various aspects, from contribution rates to benefit calculations, indicating a multi-faceted approach. Public consultations are expected to follow, allowing stakeholders and the general public to provide feedback on the proposed measures.

Key Areas of Proposed Change

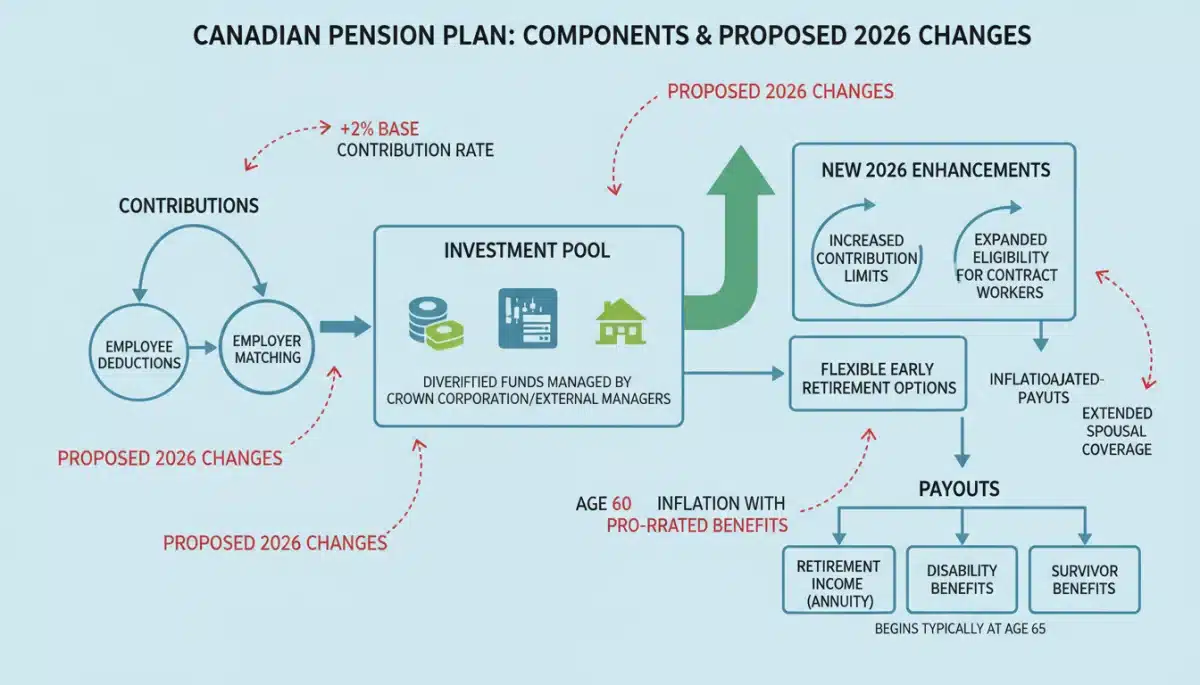

The government’s proposals for Pension Plan Reforms target several core components of the current system. These include potential adjustments to the age of eligibility for certain benefits, modifications to how benefits are calculated, and possible changes in contribution rates for employees and employers.

Initial reports suggest a recalibration of the actuarial assumptions used to forecast the plan’s financial health. This recalibration is a response to updated demographic data and economic outlooks, ensuring the plan’s projections are as accurate as possible for the coming decades.

The aim is to create a more robust and adaptable framework that can withstand future economic downturns and demographic shifts. The government emphasizes that these changes are proactive, rather than reactive, designed to secure the system’s future.

- Potential adjustments to the age of eligibility for pension benefits.

- Revisions to the formula used for calculating retirement benefits.

- Consideration of changes to employee and employer contribution rates.

- Introduction of new mechanisms to enhance pension plan flexibility.

Impact on Future Retirees’ Benefits

The proposed Pension Plan Reforms will inevitably reshape the financial landscape for Canadians planning their retirement. Future retirees, particularly those currently in their working years, will need to closely examine how these changes might affect their projected income streams and overall financial security.

While specific details are still emerging, early analyses suggest that some individuals might experience adjustments in the amount or timing of their pension payouts. This necessitates a proactive approach to personal financial planning, encouraging Canadians to review their retirement strategies in light of these potential reforms.

The government’s objective is to ensure the system remains viable, but this often means making difficult decisions that could alter individual expectations. Understanding these potential impacts early is key to informed decision-making.

Who Will Be Most Affected?

The immediate impact of the Pension Plan Reforms is expected to vary across different age groups and employment sectors.

Younger Canadians, those still decades away from retirement, may see the most significant long-term changes to their benefit entitlements and contribution requirements.

Near-retirees, individuals approaching eligibility within the next five to ten years, might also face adjustments, albeit potentially less drastic than those for younger cohorts. The government aims to minimize disruption for those closest to retirement, but some modifications could still apply.

Current retirees, who are already receiving benefits, are generally expected to be shielded from immediate cuts, as governments typically strive to protect vested benefits. However, the exact scope of protection will depend on the final legislative language.

- Younger workers (under 45) facing the most substantial long-term adjustments.

- Near-retirees (ages 55-65) potentially experiencing minor adjustments to eligibility or calculation.

- Current retirees (already receiving benefits) likely to see minimal direct impact on existing payouts.

- Self-employed individuals and small business owners may face specific changes to contribution rules.

Government Rationale and Objectives

The Canadian government’s rationale behind the Pension Plan Reforms stems from a commitment to long-term fiscal responsibility and intergenerational equity. With an aging population and shifts in workforce dynamics, the existing pension framework requires recalibration to remain sustainable and fair for all Canadians.

Officials highlight that without these proactive measures, the system could face significant strain in the decades to come. The objective is not merely to cut costs, but to fortify the foundation of the national pension plan, ensuring it can continue to serve as a cornerstone of retirement security.

The reforms are presented as a necessary evolution, reflecting a forward-thinking approach to social welfare in a changing global economic climate. Transparency and public engagement are stated priorities throughout the reform process.

Ensuring Long-Term Sustainability

A primary objective of the Pension Plan Reforms is to guarantee the long-term financial sustainability of the Canada Pension Plan (CPP). This involves ensuring that the plan’s assets are sufficient to cover its future liabilities, even amidst changing economic conditions and demographic trends.

The reforms seek to balance the contributions made by today’s workers with the benefits paid out to today’s and tomorrow’s retirees. This delicate balance is achieved through actuarial analyses that project the plan’s financial health decades into the future.

By making strategic adjustments now, the government aims to avoid more drastic measures later, which could be far more disruptive to Canadians’ retirement plans. These changes are positioned as preventative actions.

Public Consultation and Stakeholder Feedback

As part of the process for Pension Plan Reforms, the government has committed to engaging in extensive public consultation. This period is crucial for gathering feedback from various stakeholders, including labour unions, employer associations, financial experts, and individual Canadians.

The consultation phase allows for a democratic exchange of ideas, ensuring that the final legislative package reflects a broad range of perspectives and concerns. It also provides an opportunity for the public to better understand the proposed changes and their potential implications.

Transparency in this process is paramount, with the government expected to publish consultation documents and summaries of feedback received. This open dialogue aims to build public trust and ensure the reforms are well-understood and accepted.

Engagement with Key Groups

The government plans to specifically engage with key groups who will be directly affected by the Pension Plan Reforms. This includes representatives from seniors’ advocacy organizations, youth groups, and Indigenous communities, whose specific needs and concerns must be considered.

Dialogue with provincial and territorial governments is also a critical component, as the Canada Pension Plan is a shared responsibility. Harmonization and collaboration across jurisdictions are essential for successful implementation and equitable outcomes for all Canadians.

Financial institutions and advisors will also play a crucial role in providing insights and helping to disseminate information to their clients. Their expertise can help identify practical challenges and propose viable solutions for effective implementation.

- Labour unions and employer associations providing input on workforce impacts.

- Seniors’ advocacy groups ensuring the protection of current and near-retiree benefits.

- Financial experts offering actuarial and economic analyses of the proposals.

- Provincial and territorial governments collaborating on implementation strategies.

Preparing for the Pension Plan Reforms 2026

For Canadians, preparing for the Pension Plan Reforms means taking proactive steps to understand how these changes might impact their personal financial planning. It is an opportune moment to review existing retirement strategies and consider potential adjustments.

Financial advisors recommend staying informed through official government channels and reputable news sources. Understanding the timeline for implementation and any staggered effects of the reforms will be crucial for effective planning.

This period of reform serves as a reminder of the importance of diversified retirement savings and not solely relying on government-provided pensions. Exploring other savings vehicles like RRSPs, TFSAs, and private pensions becomes even more relevant.

Financial Planning Strategies

In light of the impending Pension Plan Reforms, individuals should consider several financial planning strategies. This includes reassessing their retirement goals, calculating potential shortfalls, and exploring ways to bridge any gaps that may arise from the reforms.

One key strategy involves maximizing contributions to other retirement savings vehicles. For example, increasing contributions to Registered Retirement Savings Plans (RRSPs) or Tax-Free Savings Accounts (TFSAs) can provide additional financial security independent of the CPP.

Consulting with a qualified financial advisor can provide personalized guidance tailored to individual circumstances. An advisor can help model different scenarios and recommend strategies to mitigate any negative impacts of the reforms.

- Reviewing current retirement savings and investment portfolios.

- Considering increasing contributions to RRSPs and TFSAs.

- Exploring private pension options or workplace retirement plans.

- Seeking professional advice from a certified financial planner.

Historical Context of Pension Reforms in Canada

The Pension Plan Reforms are not an isolated event but rather part of a long history of adjustments to Canada’s retirement income system. The Canada Pension Plan (CPP) itself has undergone several significant modifications since its inception in 1966, reflecting changing economic realities and societal needs.

Past reforms have often focused on ensuring the plan’s solvency, expanding benefits, or adapting to demographic shifts. These periodic reviews and adjustments are a testament to the dynamic nature of pension systems and the necessity for continuous adaptation.

Understanding this historical context helps to frame the current proposals, demonstrating that such reforms are a normal and necessary part of maintaining a robust social safety net. Each reform aims to strengthen the system for future generations.

Previous Major Changes

Previous major changes to the CPP have included enhancements to benefits, adjustments to contribution rates, and modifications to eligibility criteria. For instance, significant reforms were enacted in the late 1990s to restore the plan’s financial health, which involved a gradual increase in contribution rates and other adjustments.

More recently, the CPP enhancement, which began in 2019, aimed to increase the amount of retirement income Canadians receive through the plan. These changes highlight a continuous effort to improve the system while ensuring its long-term viability.

The current Pension Plan Reforms build upon this legacy, aiming to further refine the system to meet the challenges of the mid-21st century. Learning from past reforms informs the approach taken today.

Potential Economic and Social Implications

The Pension Plan Reforms carry significant potential economic and social implications for Canada. Economically, changes to contribution rates could affect disposable income for workers and labour costs for businesses, potentially influencing consumer spending and investment patterns.

Socially, the reforms could alter retirement behaviours, with some individuals potentially working longer or adjusting their post-retirement lifestyles. The perception of retirement security could also shift, prompting greater emphasis on personal savings and private investments.

The government will need to carefully monitor these broader impacts to ensure the reforms achieve their intended goals without creating undue hardship or unintended negative consequences for Canadian society. A balanced approach is essential.

Broader Societal Impact

Beyond individual finances, the Pension Plan Reforms could influence broader societal trends. Changes in retirement age or benefit levels might affect workforce participation rates among older Canadians, potentially altering the dynamics of the labour market.

There could also be implications for intergenerational wealth transfer and family support structures, as individuals adjust their financial planning. The reforms underscore the interconnectedness of economic policy and social well-being.

Ensuring that vulnerable populations are not disproportionately affected will be a key consideration throughout the implementation phase. Social equity and fairness remain central to the discourse surrounding these significant policy changes.

Future Outlook and Next Steps

The future outlook for Pension Plan Reforms involves a period of legislative review, public debate, and eventual implementation. The government’s proposals are currently in the initial stages, meaning there will be opportunities for further refinement and adjustment based on feedback received.

Canadians should anticipate ongoing updates from official sources as the reform process progresses. Key milestones will include the tabling of specific legislation, debates in Parliament, and the finalization of the legal framework governing the changes.

The implementation phase will likely be gradual, with various elements of the reforms coming into effect at different times leading up to and beyond 2026. This staggered approach is designed to allow individuals and institutions to adapt smoothly.

What to Expect in the Coming Months

In the coming months, Canadians can expect to see more detailed information regarding the Pension Plan Reforms. This will include specific legislative texts, detailed actuarial reports, and clearer guidance on how the changes will be applied to different demographics.

The public consultation period will be critical, offering a chance to voice concerns and contribute to the shaping of the final reforms. Engaging with these processes is an important step for anyone potentially affected by the changes.

Watching for announcements from the Department of Finance and Employment and Social Development Canada will provide the most accurate and up-to-date information. Staying informed will be key to understanding the full scope and impact of these reforms.

| Key Point | Brief Description |

|---|---|

| Proposed Changes | Government proposes adjustments to CPP to ensure long-term sustainability. |

| Impact on Retirees | Future retirees may see changes to benefit amounts, eligibility, or timing. |

| Rationale | Reforms address demographic shifts and economic factors for system solvency. |

| Next Steps | Public consultations and legislative processes to finalize the reforms. |

Frequently Asked Questions About Pension Plan Reforms 2026

The primary goals of the Pension Plan Reforms are to ensure the long-term financial sustainability of the Canada Pension Plan (CPP) and adapt it to evolving demographic and economic conditions. This includes balancing contributions with benefits for future generations of retirees.

While specific details are still under discussion, the Pension Plan Reforms may involve adjustments to the age of eligibility for certain benefits. Individuals should monitor official announcements to understand how their specific retirement timeline might be impacted by any finalized changes.

Generally, governments aim to protect vested benefits for current retirees. While the Pension Plan Reforms primarily target future benefits and contributions, it’s essential to review the final legislation for any specific provisions that might affect those already receiving payments.

To prepare for the Pension Plan Reforms, Canadians should stay informed through official government sources, review their personal retirement plans, and consider consulting a financial advisor. Diversifying savings beyond CPP is also a prudent strategy.

Official information regarding the Pension Plan Reforms will be released by the Department of Finance Canada and Employment and Social Development Canada. Their websites will provide the most accurate and up-to-date details, including consultation documents and legislative updates.

What this means

The proposed Pension Plan Reforms signal a critical juncture for Canada’s retirement income system. These changes, driven by demographic and economic shifts, aim to establish a more resilient and equitable framework for generations to come.

Canadians are encouraged to actively engage with the public consultation process and to review their personal financial strategies in light of these developments.

The coming months will bring further clarity as legislative details emerge and public feedback is integrated into the final policy, underscoring the dynamic nature of securing retirement in a changing world.