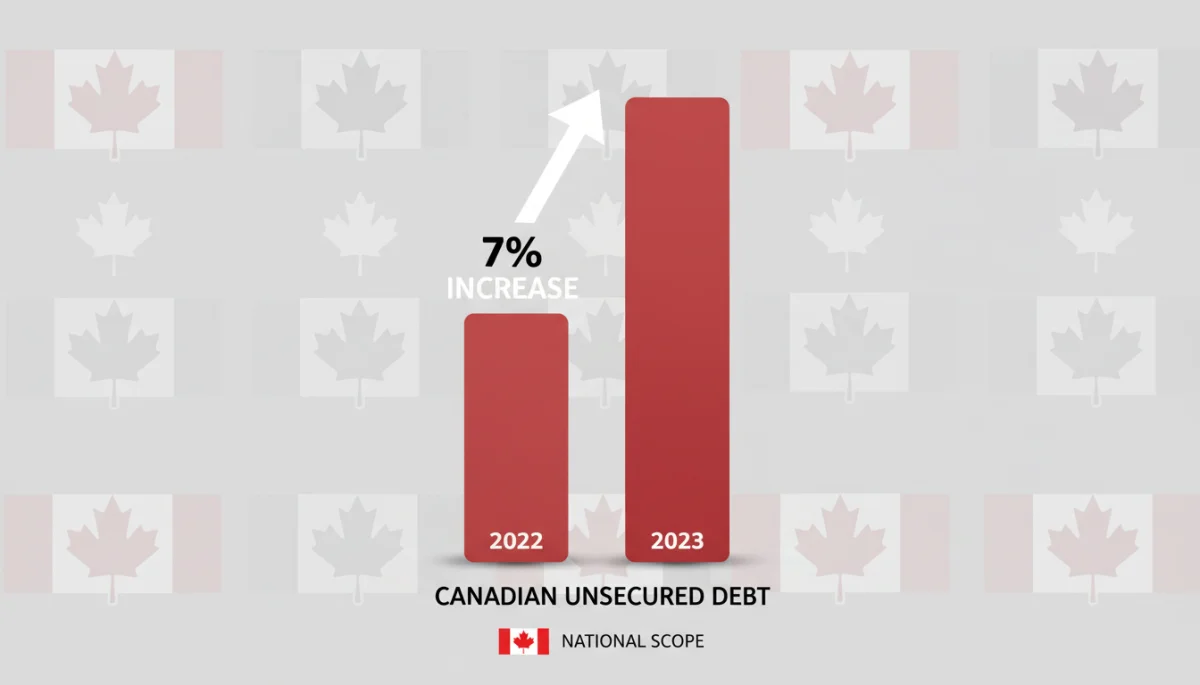

Canada’s Unsecured Debt Soars: January 2026 Report Reveals 7% Rise

In 2026, a critical report on Canadian Consumer Debt reveals a 7% surge in unsecured borrowing, signaling intense financial pressure on households nationwide.

This rise in credit card and line-of-credit usage reflects real-world struggles with the cost of living, directly impacting personal budgeting and national economic stability.

As insolvency filings reach their highest levels in over a decade, understanding these trends is essential for making informed financial decisions.

This analysis provides a clear overview of the report’s key findings, the factors driving this debt spike, and the implications for the average Canadian family.

Understanding the January 2026 Unsecured Debt Surge

The January 2026 report revealing a 7% rise in unsecured debt across Canada has sent ripples through financial circles.

This significant increase points to a growing reliance on credit cards, lines of credit, and other forms of borrowing not backed by collateral, which often carry higher interest rates and greater risk.

This surge in Canadian Unsecured Debt Rise is particularly concerning as it suggests that Canadians may be struggling to keep pace with the rising cost of living, or are perhaps taking on more debt to manage everyday expenses.

The report provides a snapshot of the nation’s financial health at the beginning of the new year, setting a cautious tone for the economic outlook.

Analyzing the data further reveals that this increase is not uniform across all demographics or regions, though the overall trend is undeniably upward.

Various factors, including inflation, stagnant wage growth, and lingering effects of previous economic downturns, are believed to be contributing to this complex financial picture for Canadians.

Key Drivers Behind the 7% Increase

Several interconnected factors appear to be driving the substantial 7% increase in Consumer Debt Levels.

Inflation, which has remained stubbornly high, continues to erode purchasing power, forcing many households to lean on credit to cover essential goods and services.

Alongside inflation, a period of rising interest rates has made borrowing more expensive, yet demand for credit has not diminished.

This creates a challenging environment where existing debt becomes harder to service, and new debt accrues at a faster pace, trapping some consumers in a cycle of increasing financial burden.

Furthermore, wage growth has, for many, not kept pace with the rising cost of living, leading to a widening gap between income and expenditure.

This disparity often compels individuals to turn to unsecured credit as a temporary solution, exacerbating the overall Canadian Unsecured Debt Rise observed in the recent report.

Inflationary Pressures and Cost of Living

- Higher prices for groceries, fuel, and housing are forcing Canadians to spend more on essentials.

- Many households are finding their disposable income significantly reduced, leading to reliance on credit for daily needs.

- The persistent inflationary environment makes it difficult for consumers to save, pushing them further into debt.

The sustained inflationary environment directly impacts consumer behaviour, making it challenging for individuals to maintain their previous lifestyles without incurring additional debt.

This pressure is felt acutely by lower and middle-income households, who often have less financial flexibility.

The cost of living crisis, therefore, is a primary catalyst for the escalating Consumer Debt Levels, highlighting a fundamental economic imbalance.

Without substantial wage increases or a significant cooling of inflation, this trend is likely to persist.

Regional Disparities in Debt Accumulation

While the 7% rise in unsecured debt is a national average, the January 2026 report indicates notable regional disparities across Canada.

Certain provinces and metropolitan areas are experiencing higher rates of debt accumulation, reflecting localized economic conditions and varying cost-of-living pressures.

For instance, urban centres with particularly high housing costs tend to show a greater reliance on unsecured credit to bridge financial gaps.

This geographical variation underscores the complex interplay of local economies, employment rates, and housing markets in shaping the overall Canadian Unsecured Debt Rise.

Understanding these regional differences is crucial for policymakers and financial advisors to tailor effective strategies that address localized challenges.

A one-size-fits-all approach may not be sufficient to mitigate the escalating Consumer Debt Levels.

Impact on Specific Demographics

The report also sheds light on how different demographic groups are affected by this rise in unsecured debt.

Younger Canadians and those with lower incomes often bear a disproportionate burden, frequently relying on credit to manage unexpected expenses or simply to make ends meet in a challenging economy.

Seniors on fixed incomes can also be particularly vulnerable to rising costs and the need for credit, especially when faced with unexpected medical expenses or home repairs.

The growing Canadian Unsecured Debt Rise therefore has broad societal implications, touching individuals from all walks of life.

These demographic insights are vital for developing targeted financial literacy programs and support systems.

Addressing the specific needs of these vulnerable groups is essential in mitigating the adverse effects of increasing Consumer Debt Levels.

Consequences for Canadian Households

The escalating Consumer Debt Levels January 2026: Report Shows a 7% Rise in Unsecured Debt Across Canada carries significant consequences for individual households.

Higher debt loads often lead to increased financial stress, impacting mental health and overall well-being. The burden of debt can also limit future financial opportunities, such as saving for a down payment or retirement.

Moreover, a rise in unsecured debt heightens the risk of default, which can severely damage credit scores and restrict access to essential financial services.

This creates a vicious cycle where individuals struggling with debt find it even harder to secure favourable terms for loans or mortgages, further entrenching their financial difficulties.

The long-term implications of this trend could see a reduction in consumer spending, as more income is allocated to debt servicing rather than consumption or investment.

This shift could have broader economic repercussions, slowing overall growth and impacting various sectors of the Canadian economy. The Canadian Unsecured Debt Rise is a clear indicator of potential economic headwinds.

Increased Financial Stress and Mental Health

- The constant worry of debt can lead to anxiety, depression, and other mental health issues.

- Financial strain often impacts relationships and overall quality of life within a household.

- Access to debt counselling and mental health support becomes increasingly critical in these circumstances.

The psychological toll of mounting debt is a serious concern that extends beyond mere financial figures.

As Consumer Debt Levels January, the associated stress levels are likely to climb, affecting productivity and societal well-being.

Addressing the mental health aspect of financial stress is just as important as providing financial relief. Holistic approaches are needed to support Canadians grappling with the pressures of increasing unsecured debt.

Government and Institutional Responses

In light of the concerning Consumer Debt Levels, both government bodies and financial institutions are expected to review their current policies and consider new interventions.

This could include tightening lending standards, offering debt relief programs, or enhancing financial literacy initiatives.

The Bank of Canada, in particular, will be closely monitoring these trends as they evaluate future monetary policy decisions, including potential adjustments to interest rates.

The aim would be to balance economic stability with the need to prevent further increases in household indebtedness.

While specific measures are yet to be fully articulated, the urgency of the situation demands a coordinated response from all stakeholders.

Proactive steps are essential to prevent the Canadian Unsecured Debt Rise from spiralling into a more severe economic crisis for many families.

Potential Policy Adjustments

Policymakers may consider a range of options, from stricter regulations on consumer lending to increased funding for credit counselling services.

The goal is to create a more resilient financial environment for Canadians, safeguarding them against the pitfalls of excessive debt.

Discussions around targeted financial aid for vulnerable populations, or even changes to bankruptcy laws, could also emerge as part of a broader strategy to address the rising Consumer Debt Levels.

Transparency and accessibility of financial information will be key.

Any policy adjustments will need to be carefully calibrated to avoid inadvertently stifling economic growth while still providing necessary protections for consumers.

The delicate balance between encouraging responsible borrowing and stimulating the economy is a challenge for legislators.

Navigating Personal Finances Amidst Rising Debt

For individual Canadians, the report on Consumer Debt Levels serves as a critical reminder to reassess personal financial strategies. Proactive debt management and budgeting are more important than ever in this economic climate.

Understanding one’s own debt profile, including interest rates and repayment terms, is the first step towards taking control.

Seeking professional advice from credit counsellors or financial planners can provide tailored strategies to reduce debt and build financial resilience against the backdrop of the broader Canadian Unsecured Debt Rise.

Focusing on reducing non-essential spending, building an emergency fund, and exploring options for consolidating high-interest debt are practical steps individuals can take.

These measures can help mitigate the personal impact of the national trend of increasing unsecured debt.

Strategies for Debt Reduction

- Create a detailed budget to track income and expenses, identifying areas for cutbacks.

- Prioritize paying down high-interest debt first, such as credit card balances.

- Consider debt consolidation options, like a lower-interest loan, to simplify payments and reduce overall interest paid.

Developing a robust personal financial plan is crucial for navigating the current economic challenges.

The rise in Consumer Debt Levels highlights the necessity for individuals to be vigilant and proactive in managing their money.

Empowering oneself with financial knowledge and adopting disciplined spending habits can significantly reduce personal vulnerability to wider economic shifts. These personal strategies form a vital defence against the increasing national debt burden.

The Role of Financial Literacy

In light of the concerning Consumer Debt Levels, the importance of financial literacy cannot be overstated. Educating Canadians about responsible borrowing, budgeting, and saving is a long-term solution to fostering greater financial stability.

Improved financial education can empower individuals to make informed decisions, avoid predatory lending practices, and understand the true cost of credit.

This foundational knowledge is essential for preventing future surges in unsecured debt and building a more financially resilient population.

Both government initiatives and community-based programs have a crucial role to play in promoting financial literacy across all age groups and demographics.

Equipping Canadians with these vital skills is a key strategy for mitigating the impacts of the current Canadian Unsecured Debt Rise.

Educational Initiatives and Resources

Various organizations across Canada offer free or low-cost resources for financial education, including workshops, online courses, and one-on-one counselling.

These resources cover topics from basic budgeting to complex debt management strategies, providing practical tools for everyday financial challenges.

Encouraging schools to integrate comprehensive financial literacy into their curricula can also lay a strong foundation for future generations.

Early education on money matters can instil good habits that prevent individuals from falling into debt traps later in life, directly addressing the underlying causes of the Consumer Debt Levels .

Accessible and engaging financial education is a powerful tool in the fight against rising debt.

By making financial knowledge a priority, Canada can foster a more financially savvy populace capable of navigating economic uncertainties with confidence.

| Key Point | Brief Description |

|---|---|

| Unsecured Debt Increase | Canada saw a 7% rise in unsecured debt by January 2026, as per a recent report. |

| Driving Factors | High inflation, stagnant wages, and rising interest rates are key contributors. |

| Household Impact | Increased financial stress, reduced savings, and higher risk of default for Canadians. |

| Mitigation Strategies | Personal budgeting, debt counselling, and financial literacy are crucial responses. |

Frequently Asked Questions About Canadian Unsecured Debt

A 7% rise in unsecured debt means many Canadians are relying more on credit cards and personal loans to manage expenses. This can lead to higher monthly payments and increased financial strain, making it harder to save or invest for the future. It signals potential challenges for household budgets nationwide.

Several factors are at play, including persistent inflation which drives up the cost of living, and wage growth that hasn’t kept pace. Additionally, higher interest rates make borrowing more expensive, exacerbating the debt burden for consumers. Economic uncertainties also lead some to rely on credit more heavily.

Rising unsecured debt can slow economic growth by reducing consumer spending power, as more income is diverted to debt servicing. It can also increase the risk of loan defaults, potentially affecting the stability of financial institutions. The overall economic health is closely tied to consumer financial well-being.

Individuals can manage debt by creating a strict budget, prioritizing high-interest debt repayment, and exploring debt consolidation options. Seeking advice from credit counsellors or financial advisors can also provide personalized strategies. Building an emergency fund is crucial to avoid future reliance on credit.

While specific new initiatives are yet to be fully announced, the government and financial regulators are likely monitoring the situation closely. Potential responses could include enhanced financial literacy programs, stricter lending guidelines, or targeted support for vulnerable populations to mitigate the impact of the rising debt.

Looking Ahead: Implications for Canadian Financial Health

The report indicating a Consumer Debt Levels January 2026: Report Shows a 7% Rise in Unsecured Debt Across Canada necessitates a vigilant approach from both consumers and policymakers.

This trend suggests that many Canadians are facing significant financial pressure, which could have lasting effects on their economic stability and future prospects.

It underscores the urgent need for robust financial planning and informed decision-making at every level.

Moving forward, it will be crucial to observe how economic conditions evolve, particularly regarding inflation and interest rates, as these will heavily influence the trajectory of Canadian unsecured debt.

The effectiveness of any governmental or institutional responses in mitigating this rise will also be a key factor to watch. Canadians should remain proactive in managing their finances and seeking support when needed.

Ultimately, addressing the challenges posed by these rising debt levels requires a multi-faceted approach, combining individual responsibility with supportive economic policies and accessible financial education.

The long-term financial health of Canadian households depends on a collective effort to understand, manage, and ultimately reduce the burden of debt.

For a deeper analysis of the structural issues at play, see the latest reporting on why debt loads continue to soar for insolvent Canadians.